|

PART THREE – AIR CHINA  A good starting point in a discussion about Air China is a brief description of the genesis of China’s “Big Four.” We can also note the absolute “rock bottom” from which China began to build an air transportation sector. The starting point is 1949, when the Communist Party took over total control of China. In that year, the Communist government established the original Civil Aviation Administration of China (“CAAC”) with the intent that CAAC would manage the totality of civil aviation in China. However, in that year civil aviation in China was nothing more than a thought. Nothing about a civil aviation sector really existed anywhere in China. The next year saw the beginning of the Korean War in which approximately 300,000 Chinese Army troops engaged the US in battle on the Korean Peninsula. That war ended in an armistice in 1953. In 1958, Mao Zedong began China’s “Great Leap Forward” which actually had no involvement with aviation in China. Then, in the time between 1959 and 1961, China lost millions of people due to the Great Famine. Historians differ on the exact number, but it is generally agreed that some 36 million Chinese people died from starvation during that famine. It was no time to try to build an airline industry. The real beginning of China’s air transportation industry began in 1963, when China purchased six Vickers Viscount aircraft from Great Britain, a four-engine turboprop that was already 15 years old at that time and certainly technologically obsolete. This purchase was immediately followed by a surprising purchase of four Hawker Siddeley Trident aircraft from Pakistan. In 1963 the Trident was a brand-new three-engine jet aircraft. And then the real turning point happened in 1972, with the Nixon visit to China. At that point, CAAC ordered 10 Boeing 707 jets.

From that point in 1972 to the year 1988, the entirety of civil aviation in China was totally controlled and managed by CAAC. In 1973, China completed its very first borrowing from Western banks for the purpose of financing aircraft. From 1973 until the present, China’s airline industry grew steadily. Then in 1988, CAAC made the decision to divide the entirety of the China civil aviation sector (rather the passenger-carrying portion) into individual carriers determined by geographical regions, which were Air China, China Eastern, China Southern, China Northern, China Southwest, and China Northwest. Eventual mergers and other developments eventually brought China to where it is today. From the beginning in 1988, Air China has been the national airline of China, i.e., the “flag carrier.” It was given the chief responsibility for international flights and its original fleet in 1988 included all of CAAC’s long haul aircraft, which were B747’s, B767’s, and B707’s. Air China was given all of the international long haul routes that CAAC operated. Air China is headquartered in Beijing, which is also its primary hub today. Its current secondary hubs are in Chengdu and Shanghai. Air China has a payroll of 50,000 employees, operating 402 aircraft. (Compare that to American Airlines with 122,300 employees and 951 aircraft.) Air China is a member of the Star Alliance. A difference between China’s major airlines and that of the US is the fact that Air China has majority control of other airlines, and some are international carriers. This list includes Air China Cargo, Air Macau, Beijing Airlines, Dalian Airlines, Shenzhen Airlines, Shandong Airlines, and Tibet Airlines. ***** Before going into the details, it is really interesting to stop here and note what is amazingly different between the world of China aviation and US aviation. This pertains to the relationship of labor versus management. China’s airlines are able to devote money and corporate energy to the benefit of competitor airlines that have no relationship to the employees of their own companies. In the U.S. collective bargaining agreements normally prohibit such subsidiary relationships. U.S. “Legacy” airline collective bargaining agreements have “Scope Clauses that pertain to and greatly limit subsidiary relationships. In contrast, the Chinese airlines do not have collective bargaining agreements. ***** Air Macau has 18 aircraft (four A319-100’s, four A320-200’s, 10 A321-200’s) and operates from Macau regionally in Mainline China (15 destinations) as well as flying to Taiwan, Japan, Vietnam, South Korea, Thailand, and the Philippines (24 destinations.) It is the “flag carrier” of Macau. Air China owns 67% of Air Macau. Beijing Airlines, not to be confused with Beijing Capital Airlines (a large low cost airline that is a subsidiary of Hainan Airlines), is 51% owned by Air China. There is basically no information available on the internet about this airline, but it appears to be a domestic carrier. Dalian Airlines operates from the city of Dalian China and has 10 B737-800 aircraft. They operate domestically to five different destinations in China. Air China owns 51%. Shenzhen Airlines is a large carrier that operates from the city of Shenzhen, which lies immediately on the border of the city of Hong Kong and is nearby to Macau. Shenzhen Airlines has a large fleet of 188 aircraft:

Shandong Airlines is a large carrier, serving more than 80 different destinations with a fleet of 118 Boeing 737 aircraft: 3 B737-700’s. 113 B737-800’s and 1 B737 MAX aircraft. Air China owns 23% of Shandong Airlines. This one can see that the total number of aircraft that are operated by Air China’s subsidiaries and affiliates is of similar size to the parent company, Air China. We have nothing like this in the U.S. But the sum of Air China, its subsidiaries and affiliates comes close to the size of American Airlines.

2 Comments

PART TWO  The context: By a wide margin only two countries in the world have combined airline fleets that are giant by current standards – the US and China. No other country comes even close. Using the concept of the “air travel market,” i.e., the total number of revenue passenger (air)miles flown, the US is now in the lead but China is expected to surpass it in just two more years. Once it passes the US, China will almost certainly stay in the lead forever. There is a difficulty in making comparisons between the US airline industry and that of China, and that is one of regulation. In the US, air operating certificates are issued and regulated by the FAA. In China, there is an analogous organization, the Civil Aviation Administration of China (“CAAC”). But there are great differences between the two countries as to how air operators are defined and regulated, and how “Operating Certificates” are issued by these two regulating agencies. The list of Chinese airlines which have a current “Air Operator Certificate” issued by CAAC includes the following categories of operators:

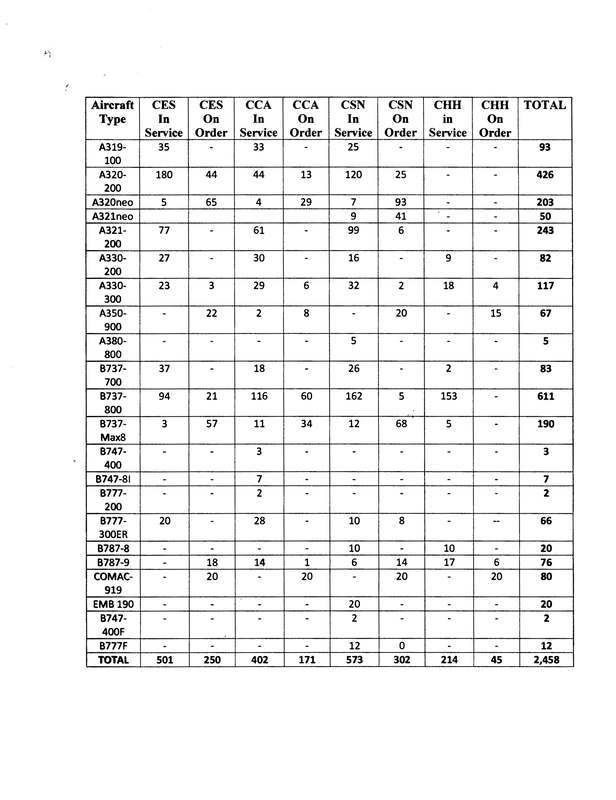

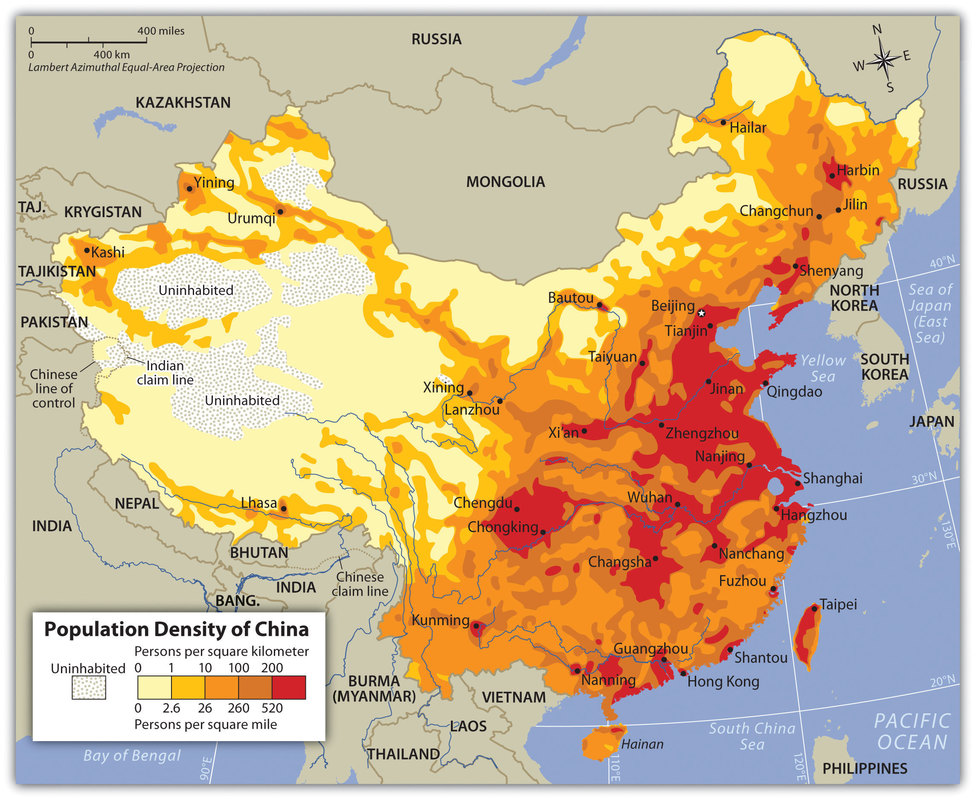

Thus, if we try to make a fair comparison between the two groups (China and the US), we must compare only apples to apples. That means we will look at the three listed China airline categories (as above) and only the Mainline US category. We simply do not have the data to examine and compare regional and commuter air travel in China to that in the U.S. The data shows us that that China has far more airlines operating large category transport aircraft than does the US. The US has fewer mainline airlines operating larger fleets. China has 22 “Domestic and International” airlines. They have 24 “Domestic” airlines, and 9 “Cargo Airlines.” In comparison, there are only 11 “Mainline” airlines holding FAA Operating Certificates in the US. But there is something much more important, and that is the fact that China’s airlines have fleets that are much younger than the US fleets. Boeing expects that China will buy more than 7,690 aircraft over the next 20 years. (This doesn’t count regional jets and crossover jets.) That means that the great majority of these aircraft additions will simply add to the overall size of the Chinese fleet, as the great majority of China’s current fleet is young. In contrast, the US airline fleet is about 13 years of age on average. When new aircraft are purchased by US airlines, the new additions will replace aircraft that will be retired. This is just another way of saying that the forecast is that the growth of China’s fleet will significantly outpace that of the US during this 20 year span. Of all of the Chinese airlines holding air operator’s certificates, nine of them are termed by the government of China to be “state operated.” But that statement requires some further definition. China’s government and its economy is centrally controlled and the government operates quite differently than the government of the US as to such things as regulation and control of industry. As an example, the Chinese government has permitted Air China (“CCA”) to be publically traded on the London, Hong Kong, and Shanghai stock exchanges. But nearly 54% of the Air China stock is owned by the China National Aviation Corporation (“CNAC”), which holds majority stakes in six other Chinese airlines and also holds minority stakes in six other Chinese airlines. Notably, CNAC is part of CAAC, which means that it is a government agency. Putting all of that together, Air China is majority owned by the government of China. Thus, Air China by any definition is government operated, government owned, government controlled, and of course government regulated. Another example is China Southern Airlines (“CSN”), which is publically traded on the New York, Shanghai, and Hong Kong stock exchanges. But China Southern Airlines is itself majority-owned by the China Southern Air Holding company, which like Air China, is majority owned by the Chinese government. Similarly, China Eastern Airlines (“CES”) is ultimately government-controlled. In direct contrast to the above is the ownership of Hainan Airlines (“CHH”), which is the fourth largest airline in China. The parent company of CHH is Grand China Air, which itself has 23 shareholders, none of which is the Chinese government. George Soros is reportedly a minority investor in Grand China Air. The two largest stockholders in Grand China Air are the HNA Group and Hainan Development Holdings. HNA has a large stock position in Hilton Worldwide. The table below provides a complete listing of the fleets of the “Big Four” airlines of China: China Eastern (CES), Air China (CCA), China Southern (CSN) and Hainan Airlines (HHN). It includes both the number and types of aircraft currently operated as well as the number and type on order. [For information, the prefix “A” denotes an Airbus aircraft and the prefix “B” denotes a Boeing aircraft.] It is also important to note that each of the Big Four airlines of China have numerous subsidiary airlines, and the numbers and types of aircraft operated by these numerous subsidiaries are not included in the table. As will be shown in subsequent postings, the numbers of aircraft operated by these subsidiaries is very large. It is also important to note that the Big Four and their subsidiaries are under some measure of control by the government of China. For example, when one or another of these airlines enters into a negotiation about the purchase of new aircraft, the Chinese government is a participant in these negotiations. China is already a prominent, if not dominant, customer for both Boeing and Airbus. Historically, dominant customers as well as launch customers of these two manufacturers have assisted in the design of new aircraft. In fact, the dominant customers usually establish the standard configuration for their various aircraft types. They also participate directly in the determination of the maintenance programs for the new aircraft. The outlook is that in the future, that role will be played by China’s airlines, which means the government of China. In Part Three of this series I will analyze in detail the “Big Four” airlines of China, beginning with Air China and its subsidiaries.  PART ONE This will be the first in a series of blog posts explaining the current and future status of China’s airline industry. Part One will focus on an examination of geographical, demographic, and economic factors that differentiate China’s from the rest of the world’s airlines. The most salient fact about China is the sheer size of its population and arguably just as important, the population density of China. First, it is a fact that one out of every four humans on Earth lives in China. Ranked by land mass, China is the second largest country on Earth, falling well below Russia in area. China is followed in size by the US, Canada, and Brazil, but both the US and Canada have a land mass that is nearly equal to that of China. On the other hand, ranked by population, China comes in as #1 by a very large margin. China has 1.4 billion people. India has 1.3 billion, the US has 327 million, Indonesia has 267 million, and the next largest is Brazil with 211 million. Thus the US with an area the same size as China has less than 1/4th of China’s population. Another distinguishing feature of China is the distribution of its population within its borders and the concentration of this huge population relative to historic centers. While some countries such as Russia with its Siberian wilderness, Brazil with its Amazon rainforest, and Canada with its Arctic frontier also have vast unpopulated areas, China is unique in that its huge population is packed into its Eastern half. In other words, while Canada’s population is confined to its south, Canada’s population is tiny compared to that of China’s.  An examination of the map above shows that there are three major areas of population concentration. The most important is the region defined by the curved line connecting Beijing (Peking), Qingdao (Tsingtao), Shanghai and Changsha . Highlights of this sector include the capital Beijing, the major coastal cities including the Imperial German colonization of Qingdao (and its Tsingtao beer), and the great Yangtze River, which connects Chongking, Wuhan, Nanjing, and Shanghai. Changsha has enormous historical importance in China, including its early relationship with Mao Zedong. Chongking and Chengdu together form a major central population center. In the South, Guangzhou (also known as Canton) and Hong Kong form a highly important economic center on the world’s stage. Also lying between Guangzhou and Hong Kong is the city of Macau.

For perspective, the straight line distance between Beijing and Hong Kong is 1,236 nautical miles, comparable to Los Angeles-Houston. But stepping backward with a broader look, if we compare China’s geography and population distribution to that of the US, consider a straight line drawn in the US from Chicago to New Orleans. Then compare that to a line drawn in China from Bautou in the North to Kunming in the South. The great majority of China’s population lies to the east of that Bautou-Kunming line. It is as though the entire population of the US were restricted to the Eastern portion, entirely East of a line from Chicago to New Orleans. Relocate all of the US cities of the Western side to the Eastern side of this line (cities such as Los Angeles, San Francisco, Seattle, Phoenix, and Denver) and then quadruple the population and have all of that in the Eastern side. In the three areas of concentration described above, the population density is between 520 people per square mile to more than 1,000 people per square mile. But that is covering the entirety of very large areas of the country, not just the major cities. (The population density of Metropolitan Los Angeles is 5,300 people per square mile.) China’s middle class is numerically larger than the middle class of the US (109 million compared to 92 million.) That said, as a percentage of the population, some 11% of all Chinese are considered to be middle class while 50% of the US population is middle class. At the same time, one out of six middle class people in the world live in China. Depending on what is used to “normalize” the economic statistics, China’s economy has already surpassed the economy of the US. and is now #1 in the world. For example, if we normalize GDP to that of the “Purchasing Power” of its citizenry, China beats the US by a wide margin. [1] China is developing its infrastructure at a staggering rate, far surpassing anything that the West has ever done or could conceivably do in the future. China is building is rail network such that in three years it will grow from 78,000 km today to more than 120,000 km in length. Sixty percent of that will be electrified. It is building airports at an astonishing rate, basically constructing entirely new large airports (capable of large airline operations) at a rate of eight airports every year. It will build some 800 new general aviation airports (hard-paved) between now and 2020. China is building a new airport in Beijing, named Daxing, to be the largest international airport in the world, having 7 runways and accommodating 100 million passengers per year. (In comparison, LAX with 4 runways accommodates 63 million per year.) By 2020, China’s airline industry will be the largest of all the nations in the world, pushing the airline industry of the US into second place, perhaps forever. More about that in Part Two. [1] What this means is that the cost of living in China is far less than that of the US. Money earned goes much further.  SkyWest Airlines has recently ordered 100 of the new Mitsubishi MRJ90 regional jets, adding 100 options for more. At the present time, these aircraft cannot be used for service with SkyWest’s Legacy airline affiliates (Delta Connection, American Eagle, and United Express.) Why? Does this foreshadow a major new shakeup of the regional airline industry? Japan’s Mitsubishi Aircraft Corporation (“MAC”) has been developing a new regional jet for the past fourteen years. This corporation is a partnership between the majority owner, Mitsubishi Heavy Industries and the minority owner, Toyota Motor Corporation. Following an earlier period of development, the MRJ concept was introduced in 2007. Since then, the MRJ has suffered significant setbacks, racking up nearly $1.28 Billion in development costs. To recoup this investment, Mitsubishi projects that it will have to sell as many as 400 MRJ aircraft. It is likely that China will present a strong marketing opportunity for sales of the Mitsubishi MRJ. According to an article published on August 27, 2018 by Aviation Week and Space Technology, MAC expects to sell 619 aircraft of the MRJ class to China in the next twenty years. The MRJ will be the first airliner designed and produced in Japan since the 1960’s, when it produced the YS-11, which was produced at a loss. Mitsubishi has developed two different models of the MRJ, the MRJ70, that has 69 to 80 seats, and the larger MRJ90, having 81 to 90 seats. There is no MRJ model under development that will be useful in the U.S. regional airlines 50-seat market. Both the MRJ70 and the MRJ90 are offered in three different versions: the Standard Model, the “ER” and the “LR” models. All but two of the six models run up against the “Scope Clause” that the U.S. Legacy carriers have with their pilot’s union. These Scope Clauses place a complete restriction on their Regional Airline Affiliates flying any aircraft with a maximum takeoff gross weight (“MTOGW”) of 86,000 pounds or higher. There have been conflicting reports about the MTOGW of the MRJ70, but according to the official Mitsubishi web site, the MRJ70 Standard comes in at 81,240 pounds and the MRJ70ER comes in at exactly 86,000 pounds. The MRJ70LR has a MTOGW of 89,000 pounds. All three of the MRJ90 models are well beyond 86,000 pounds MTOGW of the Scope Clauses. Orders for the MRJ70 model are few. In the U.S. market, Trans States has ordered 5, Sky West has ordered 7 and AeroLease has ordered 2. The MRJ90 is faring much better, with Trans States ordering 50 (with options for 50 more), Sky West ordered 100 (with 100 options) and AeroLease ordering 10 (with 10 options.) Even so, it will not be until mid-2020 that any of these aircraft will be delivered to the Regional Airlines. Mitsubishi makes some very aggressive claims in its MRJ sales literature. They say that the design is “optimized”, yielding the highest fuel efficiency, the lowest environmental impact, and the most passenger comfort among the 70 to 90 seat jets “ever to take flight.” Mitsubishi claims that the MRJ has the “lowest cost to operate of any aircraft in its class.” (This includes fuel burn and maintenance cost.) Among other claims, Mitsubishi states that its “advanced aerodynamics” produces a low-drag fuselage and tail cone, a streamlined nose, and an optimized winglet. The MRJ has a full fly-by-wire flight control system, which is arguably the most advanced in this regional jet class. Importantly, the MRJ uses the newly developed Pratt & Whitney Geared Turbofan engine, the MRJ70 using the PW1215G model and the MRJ90 using the PW1217G model. Mitsubishi claims a 20% lower fuel burn than comparable engines in this thrust class (15,600 to 17,600 pounds thrust.) One of the negative aspects of the MRJ70 and the MRJ90 is its limited range. The MRJ70 Standard has a range of only 1,020 nautical miles. The MRJ70ER has a range of 1,670 nautical miles and the MRJ70LR has a range of 2,020 nautical miles. The three versions of the MRJ90 have ranges of 1,150, 1,550, and 2,040 nautical miles respectively. In comparison, the Airbus A220-100 has a range of 3,100 nautical miles with a passenger capacity of 108 to 133 passengers. The Embraer E2 models have range capability starting at 2,150 nautical miles and going up to 2,450 nautical miles. So, even the “long range” versions of the MRJ do not meet the range of the most limited Embraer E2 models. However, considering that the target market for the MRJ is the regional airline market, and given that this market generally is a short-to-medium stage length market, the range limitation may not be as damaging as it seems. Today, the U.S. regional airlines operate jet aircraft that are the products of Canadair/Bombardier (now owned by Airbus) and Embraer (soon to have 80% Boeing ownership.) No Japanese designed and manufactured airliner has been operated in the U.S. since around 1982, when Mid-Pacific Airlines operated the YS-11 in Hawaiian service. (American Eagle also operated the YS-11.) Mitsubishi has commercial agreements with Boeing wherein MAC’s majority owner manufactures fuselage panels for the B777 and wingboxes for the B787, among other issues involving support. Now that Boeing will be supporting Embraer’s RJ products, how will that apparent conflict with the MRJ work itself out? Will Japan penetrate the U.S. aircraft market as it has in the automobile market? Given Toyota’s involvement with Mitsubishi and the MRJ, and given the top-of-the-line marketing claims of MRJ, can this happen? Will Mitsubishi move to produce a replacement for the ERJ145?  Recently, I posted comments about the Regional Airlines, Scope Clauses, and new regional aircraft. This post will provide some history for comparison purposes and specifically it will discuss aircraft that carry 50 to 76 passengers. Of great concern is that the outlook for the regional airline market is dismal unless new regional jet aircraft are developed by the aircraft manufacturers. The regional jet aircraft that are used today are almost exclusively made by two manufacturers, Brazil’s Embraer and Canada’s Bombardier. This year, Embraer has entered into an agreement with Boeing wherein Boeing will buy 80% of Embraer’s regional aircraft division. This awaits Brazilian government approval. Also, Airbus has purchased Bombardier, meaning that any future regional jet developments will be determined by Airbus. That deal is settled and complete. At the present time, there is no publically known new regional jet of the 50 seat or the 76 seat size that is under development. This segment is headed for extinction, which means that many cities will inevitably lose air service. To start, it is important to understand that the airlines try very hard to match the size of their aircraft to the size of the market. The term “market” in this sense means the city-pair of origin and destination of a specific flight or series of flights. For example, if the city pair is Los Angeles (LAX) and Phoenix (PHX), the potential number of seats that could be sold is large. The result is that airlines such as Southwest operate in that market with the B737-700, with something like 17 daily flights. That aircraft has 143 seats. (Other models of the B737 have more seats.) Another example is the city pair Los Angeles (LAX) and Reno (RNO). That flight is operated by, among others, Compass Airlines, operating as American Eagle, using the Embraer 175, which has 76 seats. Still another is the city pair Los Angeles (LAX) and San Luis Obispo (SBP). This flight is operated by United Express using a Bombardier CRJ200, which has 50 seats. There are only a handful of flights each day in this market. I am only writing about the US domestic market here, using narrow-body aircraft. International markets are even more complex, as they involve factors such as very large aircraft (the A380) and aircraft that have long range flight capability (the B-777ER) The point is that markets that utilize aircraft of 50, 76, and 143 seats are quite different, one from another. Even though the origin might be the same, such as LAX, the destination determines how big an aircraft can be used economically. Issues such as the runway length at the destination are not normally the determinative factor. Rather, it is the potential number of seats that can be sold, i.e., the LAX-San Luis Obispo market is much smaller than that of LAX-Phoenix. The Legacy and major airlines operate fleets of aircraft that are only suitable in large markets such as the LAX-PHX example. They do not operate regional jets themselves. While the 50-seat ERJ145 is still being produced by Embraer, there is no new development aircraft underway by the manufacturers to produce an entirely new 50-seat regional jet. It appears that the airline markets that can only support these small 50-seat aircraft are on a slow march to losing service altogether. What seems clear is only the 76-100 seat aircraft has a good outlook for the next 20+ years in terms of new aircraft now being built or designed. But as previously discussed, the Scope Clauses have created an immediate roadblock for this market, with respect to new aircraft offerings for the 76-100 seat regional jet. We can now ask the following questions:

Consider the markets such as Philadelphia (PHL)-Indianapolis (IND) or Philadelphia (PHL) – Milwaukee (MKE). Milwaukee is the 31st largest city in the U.S. with almost 600,000 people. Philadelphia is the 6th largest city in the U.S. with 1.6 million people. Indianapolis is the 16th largest city in the U.S. with 863,000 people. IND is a base for FedEx and also a hub for the regional carrier Republic Airlines. IND has many daily flights, but only two per day to Philadelphia. MKE has more daily flights to PHL, operated by American Airlines through Republic/American Eagle, Piedmont Airlines/American Eagle. Also, United through its affiliate Air Wisconsin/United Express and Delta, through SkyWest/Delta Connection all fly regional jets to PHL. The American Eagle non-stops are served by the EMB145 (same as ERJ145). United Express does not fly non-stop to and from MKE in the PHL market and they use either the ERJ145, the CRJ200, or the EMB175 in multi-stop connections. There are two issues here: one, the number of daily fights in the above two markets involving Philadelphia are relatively few. Second, the regional jet aircraft currently in use in these two markets are both too small (both the ERJ145 and the CRJ200) and getting long–in-the-tooth, meaning that they are likely on their final years of service in this market. The only new regional jets that are being developed, such as the Embraer E175 E2 and the Airbus A200-100, will not be usable under the current schedules in these two markets (and many others) as just explained. In fact, unless the Scope Clauses get amended, the regionals are heading for a cliff. Importantly, the aircraft manufacturers that will design and build new regional jets have been reduced to just Boeing and Airbus, although Japan’s Mitsubishi and China are trying to get into the regional jet market. Still, there is no manufacturer that is working on a replacement for the ERJ145 and the CRJ200.  The above image shows the ERJ145 in United Nations livery.

Last week, 29 year-old Richard Russell stole a Horizon Air Q400 airplane and took off from SEA-TAC airport where he worked as a ground service operator. Before fatally crashing more than an hour later, he went on a joyride complete with impressive acrobatic maneuvers. It has been reported that his only prior experience was playing videogames. In the aftermath of the incident, there has been much discussion in the media about possible courses of action to remedy such a situation, i.e., where the bad actor is enabled by experience, sufficient knowledge and privileged access. Without that convergence, an average person would not have been able to pull off the theft, flight, and crash. Some of the proposals have been draconian, others merely impractical. To evaluate them and come up with an appropriate but measured response, it’s instructive to review analogous incidents. In the past, serious and even murderous events have taken place with similar elements to the Richard Russell case. This blog will lay out some of them. EgyptAir Flight 990, October 31, 1999. The flight involved a Boeing 767-366ER, enroute from JFK to Cairo. There were 247 people on board. Approximately 62 nautical miles South of Nantucket, beginning from an enroute altitude of 33,000 feet, the First Officer, alone in the cockpit (the Captain was in the lavatory), pushed the aircraft’s nose down into a near-vertical dive, shut off the engines, and crashed the B767 into the Atlantic Ocean. All on board perished and the aircraft was completely demolished on impact with the sea. Nothing significant was recovered, only small pieces of debris. No bodies were found, only small body parts that allowed some limited forensic identification. The final “Probable Cause” was a suicidal act on the part of the First Officer. He murdered 247 people. Germanwings Flight 9525, March 24, 2015. This is so recent that likely many readers will remember the accident. The flight involved an Airbus A320-211 that was enroute from Barcelona to Dusseldorf. Flying in a mountainous region some 62 nautical miles north-west of Nice (Alpes-de-Haute-Provence), the First Officer was (as in the EgyptAir case) alone in the cockpit with the Captain having left the cockpit. The First Officer locked the Captain out of the cockpit, started a descent from an enroute altitude of 38,000 feet, and crashed the aircraft into a mountain. The investigation concluded that the First Officer was suicidal. He murdered all 50 people who were on board the aircraft. August 21, 2015 Thalys Train 9364 Attack. Train 9363, traveling from Amsterdam to Paris, having just crossed the border from Belgium to France, was attacked by a 25-year old Moroccan man armed with an AKM assault rifle and 9mm Luger pistol. He also had a bottle of gasoline and a box cutter in his possession. He carried a total of 270 rounds of ammunition. In an almost miraculous fortuity, the attacker was encountered by two young male passengers with military training who intervened. There was an initial struggle and some gunfire, but the attacker was finally subdued. There were no fatalities, but 3 train passengers were injured. The attacker was also injured and he was apprehended. The Bastille Day Truck Attack. On July 15, 2016, a 31-year old French Tunisian man drove a truck down a crowded seafront street in Nice during a festive event on Bastille Day. He mowed down and murdered 84 people. In addition to the fatalities, another 202 people were injured in the attack, including 25 on life support and 52 in critical condition in the aftermath. This attack followed two earlier terrorist attacks within a year’s time in France, i.e., the Charlie Hebdo killings and the Bataclan massacre of 130 people in Paris. Venice California Boardwalk Attack. On August 3, 2013, a young man was able to evade roadblocks and drive his car onto the Venice Beach “boardwalk”, a place where cars aren’t permitted. It was during a typical summer afternoon, and there were hundreds of people walking lazily on the boardwalk and attending the café’s there. The aftermath was horrifying and very bloody. At least 12 people were seriously injured, 10 of them hospitalized. Although only one death resulted from the attack, it could have been much worse. Cessna 525 Crash, Payson, Utah, two days ago. At 2:30 AM in Payson Utah, a city some 60 miles south of Salt Lake City, the pilot intentionally flew a Cessna 525 into his own home, where his wife and a child were sleeping in the home. The pilot, Duane Youd, died in the crash but his wife and child were uninjured. Youd had just hours earlier been arrested for assaulting his wife, but had been released from custody before going up in the plane. The above examples are by no means complete. For example, recall the October 31, 2017 attack on the West Side Highway bicycle path of New York where a man drove a truck into a crowd and killed 8 people. After these disasters, a number of responses have been tried. For example, many airlines forbid its pilots to exit the cockpit, leaving behind just a single person. (However this restriction did not find its way into US Federal Regulations.) Police security has been increased, and some screening equipment has been installed in public places such as train stations. There will be much discussion coming in the next weeks and months. However, it is important that we all remember the past as we try to construct new remedies.  The photo above shows a Horizon Air Q400 of the same type as the stolen and crashed aircraft.

Aircraft manufacturers are doing everything that they can do to reduce fuel consumption while at the same time reducing GHG emissions without increasing the cost to operate their passenger aircraft. In the United States, only three airlines are referred to as “Legacy Airlines.” They are American, Delta, and United. Other airlines such as Southwest Airlines are termed “Major Airlines” but do not carry the “Legacy” distinction. One distinguishing characteristic of the Legacy Airlines is that they exclusively have Collective Bargaining Agreements (“CBA’s) with their pilots that incorporate provisions termed “Scope Clauses.” The Scope Clause provisions limit the Legacy Airlines in their ability to contract with independent regional airlines for cooperative services to and from the smaller airports. It is also important to understand that fundamental airline economic factors create a direct link between the size of the aircraft and the airport it serves. Smaller airports require smaller aircraft. Small airports cannot economically support large aircraft. Thus the Legacies want to “contract out” small airport services to the regional airlines that operate smaller aircraft. Importantly the regional airlines pay their pilots significantly less money that the Legacies pay their pilots. Scope Clauses limit a significant number of parameters that are defined within the contracts between the Legacies and the Regionals. For example, Scope Clauses restrict the number of seats that the regional partner aircraft can sell in each particular aircraft. Also limited are the number of aircraft in total that can be covered by these contracts. Another limitation involves the total number of hours contracted and the percentage of contracted flights that exceed certain distances. (There are other limitations as well, described later in this blog post.) Regarding seat limitations, they are placed on the number of seats that any individual aircraft is scheduled to fly. For example, the regionals operate aircraft such as the Bombardier CRJ 900. It is actually certified by the regulatory authorities to carry up to 90 passengers but the Scope Clauses restrict the operation of this aircraft to 76 seats. This specific example is in place with SkyWest Airlines’ contract with Delta Airlines for the “Delta Connection.” The SkyWest Airlines CRJ900 therefore operates with 14 empty seats in its Delta Connection contract. The seat limitation is trifurcated into the following seating limitations: Not to exceed 50 seats. SkyWest Airlines operates the Bombardier CRJ100 and the CRJ200 for American Airlines’ “American Eagle” and for Delta Airlines’ “Delta Connection.” These two aircraft are certified for just 50 seats. Between 51 and 76 seats. Skywest Airlines operates the Bombardier CRJ700 for American Eagle, The Delta Connections, and also for United Airlines’ “United Express.” The CRJ700 is certified for up to 78 seats. However, the Delta Scope Clause places restrictions at both 70 seats and 76 seats. The American Airlines Scope Clause has restrictions at 65 seats. United Airlines’ restrictions exist at a total not to exceed of 255 aircraft between 51 and 76 seats and not to exceed 153 aircraft at specifically 76 seats. Specifically, at 76 seats. SkyWest Airlines operates the Bombardier CRJ900 for the Delta Connection, with the seating configuration “blocked out” at 76 seats although the aircraft is actually certified to carry up to 90 passengers. Thus the Delta Connection operates the CRJ900 with 14 empty seats. SkyWest also operates the Embraer 175 for The Delta Connection and United Express. The EMB175 is certified for up to 88 passengers but both Delta Connection and United Express operate it in a dual class configuration, certified at 76. There are many more Regional Airlines other than Skywest Airlines that contract with the Legacies through their Scope Clauses. For example, American Airlines’ American Eagle contracts with Compass Airlines, Envoy Air, Express Jet, Mesa Airlines, Piedmont Airlines, PSA Airlines, Republic Airlines, and Trans State Airlines. The Delta Connection includes Compass Airlines, Endeavor Air, Express Jet, Go Jet, and Republic, in addition to SkyWest. The United Express includes Air Wisconsin, Commutair, Express Jet, Go Jet, Mesa Airlines, Republic Airlines, Trans State Airlines, in addition to SkyWest. The collection of all these Regional Airline operations under the three Scope Clauses are very similar to what is described above in the seating limitation trifurcation. And now we come to the 86,000 pound question. In addition to the restrictions on number of seats, total aircraft fleets, hours that can be contracted, and geographical/distance limitations, there is one remaining limit that has become a significant issue, and that is an upper limit on the “Maximum Takeoff Gross Weight” (“MTOGW”) of any aircraft that can be contracted out to the regionals. The mystery is “why” this additional restriction was interjected into the Scope Clauses and why the original restrictions were not fully determinative. What was missing? This restriction has now become a major international problem as well as hampering future regional jet sales. The parameter MTOGW incorporates the structural weight of the aircraft and its components, including engines. It also includes the weight of the passengers, their baggage, cargo, and the total weight of the fuel on board. So a limitation on MTOGW involved some limitations on or any of these measures. In any event, it limits the aircraft’s performance envelope. There are some 15 discrete, existing aircraft that can be included within the “Regional Jet” category, with the additional categorization that they are all either close to or heavier than the 86,000 pound MTOGW limit. (For example, the EMB145 has a 48,500 pound MTOGW, although not really relevant here.) Of these 15 “heavier” regional jets, only two can meet the 86,000 pound MTOGW Scope Clause restriction – the Bombardier CRJ900LR and the Embraer 170, coming in at 84,500 pounds and 85,098 pounds respectively. The AirbusA220-100, one of the Bombardier CS Series aircraft, a subject of one of my earlier blogs, has a MTOGW of 134,000 pounds. With no fuel on board, it has a maximum zero fuel weight of 100,000 pounds. The A220 is therefore totally excluded by the Scope Clause from the Legacy/Regional cooperative market. So, virtually all of the newer regional jets are being blocked out by the existing Scope Clauses. It is clear that Delta, in placing its order for the A220, intends to operate this aircraft within its own CBA. It will eventually replace the B717 that Delta currently operates. At the moment, the single aircraft that is causing the biggest problem is the Embraer 175E2, which has a MTOGW of 98,767 pounds, thus being 6 tons “overweight.” Embraer cannot reasonably be expected to address this 6 ton problem through a reduction of fuel, passengers, or cargo/baggage. Therefore, it has to look to the aircraft structure itself, but that is not doable either. Embraer is therefore actually looking at the possibility of somehow getting a waiver or elimination of the 86,000 pound MTOGW Scope Clause restriction. Epitomized by the Airbus A220 series and the Embraer E2 series, these new aircraft have greatly improved performance capabilities. They are significantly more fuel efficient, they have significantly better payload/range capabilities, and they have significant emission improvements compared to their derivative predecessors. As an example, the Embraer 175E2 burns significantly less fuel than its predecessor, the E175. To get that performance, Embraer made significant changes to the fuselage and the wing, reducing weight and improving aerodynamics. To get the reduced fuel burn, they changed the engine to an entirely new, highly advanced engine, switching from GE to Pratt & Whitney. But that engine added significant weight to the aircraft. Getting the improved fuel burn required design changes to the engine that added weight. Will the Legacy pilots agree to relax or waive the 86,000 Scope Clause restriction? Stay tuned.  The photo above shows an American Eagle CRJ700. The aircraft is actually registered to and owned by American Airlines Inc.

The three images above show the Airbus A320 assembly line at Mobile AL and how these major assemblies are moved and joined. The assemblies arrive by ship and are moved by truck to the former US Air Force Base, Brookley Field, which is 4 miles from the harbor.

Airbus has been very open and public about their criticism that the production costs for the A220 are far too high to permit the survival of the program. Airbus wants at least a 10% cost savings in these productions costs. Openly stated, the Airbus plan is to achieve this cost reduction by means of its superior negotiating capabilities with the suppliers. This remains to be seen. Airbus does not clearly say that they will squeeze cost savings out of Bombardier, be that Belfast, Quebec or Montreal, but that might have to be the case for such a reduction to be achieved. A key strategy in the Airbus acquisition of Bombardier and its CSeries aircraft was that Airbus will relocate the major fraction of A220 assembly to Mobile AL, where Airbus already assembles the A321. When Airbus opened its production line at Mobile, the company publically stated that the move was not intended to save production costs, rather the company said that the intention was not to increase costs due to the more costly logistics path. The trade-off was to be found in reduced labor costs with non-union labor in Alabama. The transportation costs would thus be offset by labor savings. Similar to the highly distributed fabrication locations that exist for the A220, major assemblies for the A320 series are fabricated at many locations as well. The A320‘s wings are made in Broughton Wales. (Similar to the case with the Northern Ireland fabrication plant for the A220, this will bring Brexit complications.) The A320 front fuselage is made in Saint-Nazaire France, and the aft fuselage in Hamburg Germany. The vertical stabilizer is made in Getafe Spain. Airbus currently operates a total of eight final assembly lines: five in France, and one each in Germany, China, and the US. If the construction of the A220 wing has to be removed entirely from Belfast and started anew somewhere in the EU, that will add at least temporary new costs. If the Chinese production of the A220 center fuselage has to be moved elsewhere for whatever reason, that will also be costly. Thus, it is hard to see where a 10% production cost will be found. What’s left are the engines (Pratt & Whitney), the avionics (Rockwell Collins), to a lesser extent, Parker Hannifin, and Liebherr Aerospace. That doesn’t seem promising.   The two photos above show fuselage sections being fabricated at Shenyang China.

The Trump Administration has imposed or threatened tariffs on imports from the EU, Canada, and China, all countries which are a part of the critical supply chain for the A220. But the real problem does not lie exclusively at the top of the supply chain but rather applies equally at the roots, at the bottom. That includes raw materials such as metals. At the present time, there is no discussion coming from the Trump Administration of the imposition of import tariffs on either entire aircraft or on major assemblies, such as the A220 center fuselage assembly coming to the Mobile facility from Shenyang China. Might that happen? The supply of metal and a myriad of raw materials from abroad could be seriously disrupted by a trade war. While imports between countries outside of the US may not be affected, a trade war (especially with China) would certainly affect the development of the Mobile plant, which is critical to the success of the A220. It is interesting to consider Shenyang. Besides making fuselage sections for the A220, this company is the only manufacturer for the vertical tail leading edge for the Boeing 787. It also makes numerous structural components for the A320 series. Shenyang is also the manufacturer of numerous military aircraft for the PRC Army, including fighters and bombers. It is easy to understand that if China-US free trade is endangered (both imports to China and exports from China) that the logistics chain for aircraft production (both Boeing and Airbus) would be impacted. Contracting with Shenyang to produce these important structural components is actually an inducement (or a concession) that encourages China to buy Boeing and Airbus aircraft. It is also an avenue through which China has acquired new technical expertise. Would a trade war between the US and China spill over into a production disruption for the A220? It is possible. Even though the original CSeries deal was between Canada and China, and now the surviving A220 is between Airbus and China, the China-US trade dispute is certainly in play, especially with a Mobile AL production facility.   The two photos shown above were taken at the Short Brothers Facility in Belfast and show the fabrication of the A220 wing.

At the present time (pending the development of an additional production line to the existing Airbus A320 plant at Mobile Alabama) the A220 assembly facility in Canada receives basically all parts of the aircraft from distant foreign suppliers. The wings, engine nacelles, and composite empennage structures are all manufactured at Short Brothers’ facility in Belfast, which is the capital of Northern Ireland. Short Brothers (“Shorts”) has been designing and manufacturing aircraft since 1908 and it was the world’s first company to make production aircraft. Shorts was bought outright by Bombardier in 1989. The total production distribution for the A220 is complex. Shenyang Aircraft Corporation of China builds the center fuselage. The aft fuselage and cockpit is manufactured in Quebec Canada, while the final assembly is in Montreal. Other major suppliers include Rockwell Collins for most of the avionics, Alenia Aeronautica of Italy for the composite horizontal and vertical stabilizers, Parker Hannifin and United Technologies of the US, and Liebherr Aerospace of Germany. The engines are Pratt & Whitney PW1500G’s. The production line at Mirabel Montreal is required by the Airbus contract to remain online until at least 2041. The Mobile production line is scheduled to make its first delivery in 2020. The production rate at Mobile is scheduled to top off at 8 per month while Mirabel is scheduled to achieve 10 per month. Given that there are already three significant orders by U.S. buyers (JetBlue, Delta, and David Neeleman) it is unclear how these orders will be split between Mirabel and Mobile. As Brexit comes to a conclusion, Northern Ireland will be departing the EU along with the UK itself. This development is one of the major unanswered questions of the Brexit negotiations. An even more troubling development is how Airbus itself will change and adapt to Brexit. [Airbus is a European Corporation, partially owned by the governments of France, Germany, and Spain. It is registered in the Netherlands and its stock trades in Germany, France, and Spain.] Airbus CEO Tom Ender has been quoted in the July 29 issue of Aviation Week & Space Technology as saying “A hard Brexit would be catastrophic….the effects….would be enormous.” Importantly, Mr. Enders said that “…certification of thousands of parts would be in question overnight.” Thus the scheme of having Belfast continue to manufacture the critical parts of the A220, such as the wing, leads to very critical uncertainties. At the very least, if the Belfast production line has to be terminated and replaced, this will bring significant difficulties to the program. Beyond that because of Brexit, Airbus itself is heading into uncertain territory, which likely will affect the market for its new aircraft such as the A220. |

Categories |

RSS Feed

RSS Feed

Live Chat Support

×

Connecting

You:

::content::

::agent_name::

::content::

::content::

::content::