|

PART THREE – AIR CHINA  A good starting point in a discussion about Air China is a brief description of the genesis of China’s “Big Four.” We can also note the absolute “rock bottom” from which China began to build an air transportation sector. The starting point is 1949, when the Communist Party took over total control of China. In that year, the Communist government established the original Civil Aviation Administration of China (“CAAC”) with the intent that CAAC would manage the totality of civil aviation in China. However, in that year civil aviation in China was nothing more than a thought. Nothing about a civil aviation sector really existed anywhere in China. The next year saw the beginning of the Korean War in which approximately 300,000 Chinese Army troops engaged the US in battle on the Korean Peninsula. That war ended in an armistice in 1953. In 1958, Mao Zedong began China’s “Great Leap Forward” which actually had no involvement with aviation in China. Then, in the time between 1959 and 1961, China lost millions of people due to the Great Famine. Historians differ on the exact number, but it is generally agreed that some 36 million Chinese people died from starvation during that famine. It was no time to try to build an airline industry. The real beginning of China’s air transportation industry began in 1963, when China purchased six Vickers Viscount aircraft from Great Britain, a four-engine turboprop that was already 15 years old at that time and certainly technologically obsolete. This purchase was immediately followed by a surprising purchase of four Hawker Siddeley Trident aircraft from Pakistan. In 1963 the Trident was a brand-new three-engine jet aircraft. And then the real turning point happened in 1972, with the Nixon visit to China. At that point, CAAC ordered 10 Boeing 707 jets.

From that point in 1972 to the year 1988, the entirety of civil aviation in China was totally controlled and managed by CAAC. In 1973, China completed its very first borrowing from Western banks for the purpose of financing aircraft. From 1973 until the present, China’s airline industry grew steadily. Then in 1988, CAAC made the decision to divide the entirety of the China civil aviation sector (rather the passenger-carrying portion) into individual carriers determined by geographical regions, which were Air China, China Eastern, China Southern, China Northern, China Southwest, and China Northwest. Eventual mergers and other developments eventually brought China to where it is today. From the beginning in 1988, Air China has been the national airline of China, i.e., the “flag carrier.” It was given the chief responsibility for international flights and its original fleet in 1988 included all of CAAC’s long haul aircraft, which were B747’s, B767’s, and B707’s. Air China was given all of the international long haul routes that CAAC operated. Air China is headquartered in Beijing, which is also its primary hub today. Its current secondary hubs are in Chengdu and Shanghai. Air China has a payroll of 50,000 employees, operating 402 aircraft. (Compare that to American Airlines with 122,300 employees and 951 aircraft.) Air China is a member of the Star Alliance. A difference between China’s major airlines and that of the US is the fact that Air China has majority control of other airlines, and some are international carriers. This list includes Air China Cargo, Air Macau, Beijing Airlines, Dalian Airlines, Shenzhen Airlines, Shandong Airlines, and Tibet Airlines. ***** Before going into the details, it is really interesting to stop here and note what is amazingly different between the world of China aviation and US aviation. This pertains to the relationship of labor versus management. China’s airlines are able to devote money and corporate energy to the benefit of competitor airlines that have no relationship to the employees of their own companies. In the U.S. collective bargaining agreements normally prohibit such subsidiary relationships. U.S. “Legacy” airline collective bargaining agreements have “Scope Clauses that pertain to and greatly limit subsidiary relationships. In contrast, the Chinese airlines do not have collective bargaining agreements. ***** Air Macau has 18 aircraft (four A319-100’s, four A320-200’s, 10 A321-200’s) and operates from Macau regionally in Mainline China (15 destinations) as well as flying to Taiwan, Japan, Vietnam, South Korea, Thailand, and the Philippines (24 destinations.) It is the “flag carrier” of Macau. Air China owns 67% of Air Macau. Beijing Airlines, not to be confused with Beijing Capital Airlines (a large low cost airline that is a subsidiary of Hainan Airlines), is 51% owned by Air China. There is basically no information available on the internet about this airline, but it appears to be a domestic carrier. Dalian Airlines operates from the city of Dalian China and has 10 B737-800 aircraft. They operate domestically to five different destinations in China. Air China owns 51%. Shenzhen Airlines is a large carrier that operates from the city of Shenzhen, which lies immediately on the border of the city of Hong Kong and is nearby to Macau. Shenzhen Airlines has a large fleet of 188 aircraft:

Shandong Airlines is a large carrier, serving more than 80 different destinations with a fleet of 118 Boeing 737 aircraft: 3 B737-700’s. 113 B737-800’s and 1 B737 MAX aircraft. Air China owns 23% of Shandong Airlines. This one can see that the total number of aircraft that are operated by Air China’s subsidiaries and affiliates is of similar size to the parent company, Air China. We have nothing like this in the U.S. But the sum of Air China, its subsidiaries and affiliates comes close to the size of American Airlines.

1 Comment

PART TWO  The context: By a wide margin only two countries in the world have combined airline fleets that are giant by current standards – the US and China. No other country comes even close. Using the concept of the “air travel market,” i.e., the total number of revenue passenger (air)miles flown, the US is now in the lead but China is expected to surpass it in just two more years. Once it passes the US, China will almost certainly stay in the lead forever. There is a difficulty in making comparisons between the US airline industry and that of China, and that is one of regulation. In the US, air operating certificates are issued and regulated by the FAA. In China, there is an analogous organization, the Civil Aviation Administration of China (“CAAC”). But there are great differences between the two countries as to how air operators are defined and regulated, and how “Operating Certificates” are issued by these two regulating agencies. The list of Chinese airlines which have a current “Air Operator Certificate” issued by CAAC includes the following categories of operators:

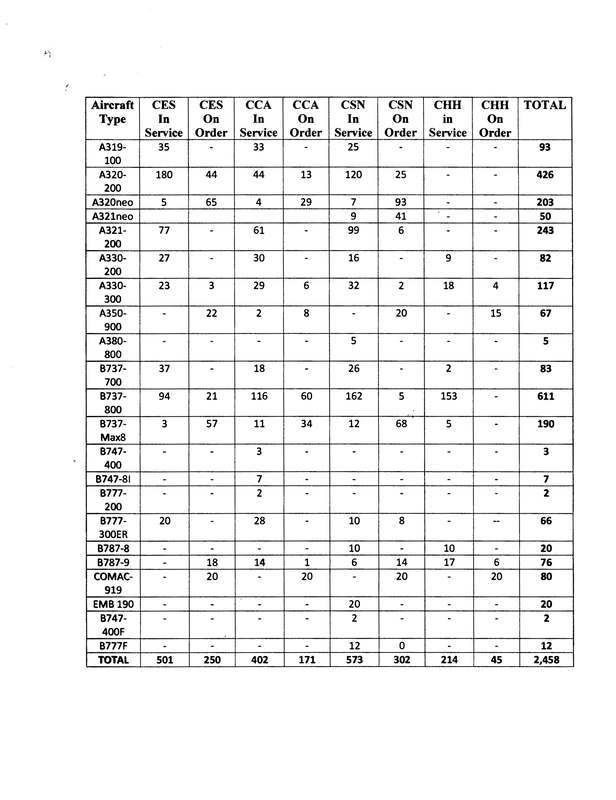

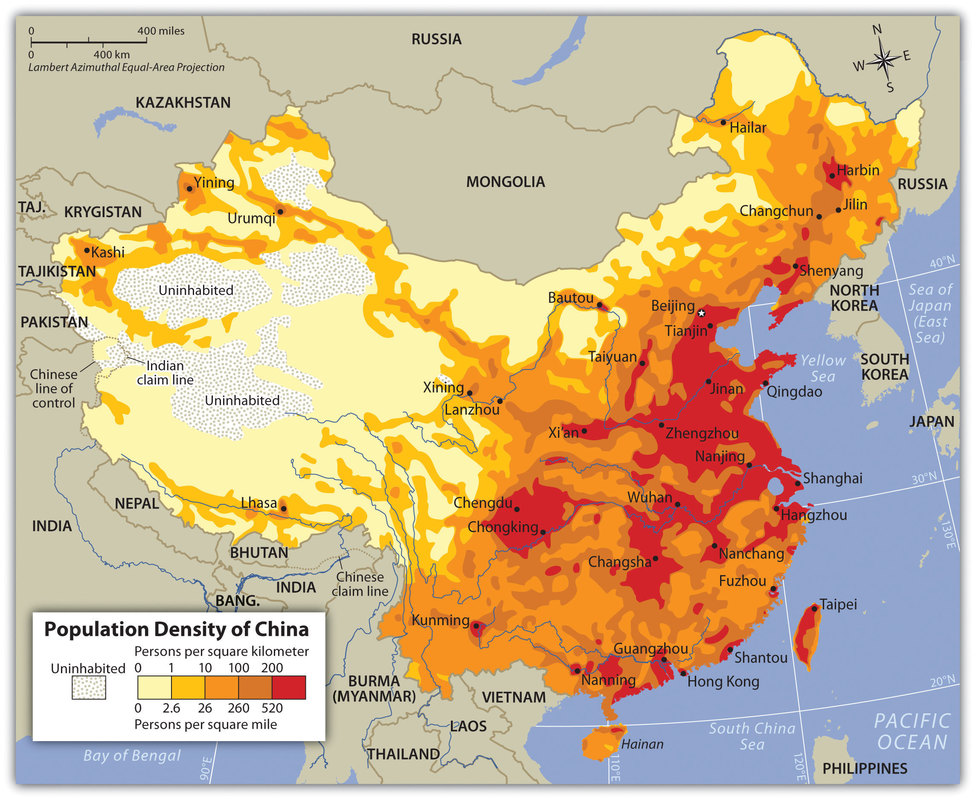

Thus, if we try to make a fair comparison between the two groups (China and the US), we must compare only apples to apples. That means we will look at the three listed China airline categories (as above) and only the Mainline US category. We simply do not have the data to examine and compare regional and commuter air travel in China to that in the U.S. The data shows us that that China has far more airlines operating large category transport aircraft than does the US. The US has fewer mainline airlines operating larger fleets. China has 22 “Domestic and International” airlines. They have 24 “Domestic” airlines, and 9 “Cargo Airlines.” In comparison, there are only 11 “Mainline” airlines holding FAA Operating Certificates in the US. But there is something much more important, and that is the fact that China’s airlines have fleets that are much younger than the US fleets. Boeing expects that China will buy more than 7,690 aircraft over the next 20 years. (This doesn’t count regional jets and crossover jets.) That means that the great majority of these aircraft additions will simply add to the overall size of the Chinese fleet, as the great majority of China’s current fleet is young. In contrast, the US airline fleet is about 13 years of age on average. When new aircraft are purchased by US airlines, the new additions will replace aircraft that will be retired. This is just another way of saying that the forecast is that the growth of China’s fleet will significantly outpace that of the US during this 20 year span. Of all of the Chinese airlines holding air operator’s certificates, nine of them are termed by the government of China to be “state operated.” But that statement requires some further definition. China’s government and its economy is centrally controlled and the government operates quite differently than the government of the US as to such things as regulation and control of industry. As an example, the Chinese government has permitted Air China (“CCA”) to be publically traded on the London, Hong Kong, and Shanghai stock exchanges. But nearly 54% of the Air China stock is owned by the China National Aviation Corporation (“CNAC”), which holds majority stakes in six other Chinese airlines and also holds minority stakes in six other Chinese airlines. Notably, CNAC is part of CAAC, which means that it is a government agency. Putting all of that together, Air China is majority owned by the government of China. Thus, Air China by any definition is government operated, government owned, government controlled, and of course government regulated. Another example is China Southern Airlines (“CSN”), which is publically traded on the New York, Shanghai, and Hong Kong stock exchanges. But China Southern Airlines is itself majority-owned by the China Southern Air Holding company, which like Air China, is majority owned by the Chinese government. Similarly, China Eastern Airlines (“CES”) is ultimately government-controlled. In direct contrast to the above is the ownership of Hainan Airlines (“CHH”), which is the fourth largest airline in China. The parent company of CHH is Grand China Air, which itself has 23 shareholders, none of which is the Chinese government. George Soros is reportedly a minority investor in Grand China Air. The two largest stockholders in Grand China Air are the HNA Group and Hainan Development Holdings. HNA has a large stock position in Hilton Worldwide. The table below provides a complete listing of the fleets of the “Big Four” airlines of China: China Eastern (CES), Air China (CCA), China Southern (CSN) and Hainan Airlines (HHN). It includes both the number and types of aircraft currently operated as well as the number and type on order. [For information, the prefix “A” denotes an Airbus aircraft and the prefix “B” denotes a Boeing aircraft.] It is also important to note that each of the Big Four airlines of China have numerous subsidiary airlines, and the numbers and types of aircraft operated by these numerous subsidiaries are not included in the table. As will be shown in subsequent postings, the numbers of aircraft operated by these subsidiaries is very large. It is also important to note that the Big Four and their subsidiaries are under some measure of control by the government of China. For example, when one or another of these airlines enters into a negotiation about the purchase of new aircraft, the Chinese government is a participant in these negotiations. China is already a prominent, if not dominant, customer for both Boeing and Airbus. Historically, dominant customers as well as launch customers of these two manufacturers have assisted in the design of new aircraft. In fact, the dominant customers usually establish the standard configuration for their various aircraft types. They also participate directly in the determination of the maintenance programs for the new aircraft. The outlook is that in the future, that role will be played by China’s airlines, which means the government of China. In Part Three of this series I will analyze in detail the “Big Four” airlines of China, beginning with Air China and its subsidiaries.  PART ONE This will be the first in a series of blog posts explaining the current and future status of China’s airline industry. Part One will focus on an examination of geographical, demographic, and economic factors that differentiate China’s from the rest of the world’s airlines. The most salient fact about China is the sheer size of its population and arguably just as important, the population density of China. First, it is a fact that one out of every four humans on Earth lives in China. Ranked by land mass, China is the second largest country on Earth, falling well below Russia in area. China is followed in size by the US, Canada, and Brazil, but both the US and Canada have a land mass that is nearly equal to that of China. On the other hand, ranked by population, China comes in as #1 by a very large margin. China has 1.4 billion people. India has 1.3 billion, the US has 327 million, Indonesia has 267 million, and the next largest is Brazil with 211 million. Thus the US with an area the same size as China has less than 1/4th of China’s population. Another distinguishing feature of China is the distribution of its population within its borders and the concentration of this huge population relative to historic centers. While some countries such as Russia with its Siberian wilderness, Brazil with its Amazon rainforest, and Canada with its Arctic frontier also have vast unpopulated areas, China is unique in that its huge population is packed into its Eastern half. In other words, while Canada’s population is confined to its south, Canada’s population is tiny compared to that of China’s.  An examination of the map above shows that there are three major areas of population concentration. The most important is the region defined by the curved line connecting Beijing (Peking), Qingdao (Tsingtao), Shanghai and Changsha . Highlights of this sector include the capital Beijing, the major coastal cities including the Imperial German colonization of Qingdao (and its Tsingtao beer), and the great Yangtze River, which connects Chongking, Wuhan, Nanjing, and Shanghai. Changsha has enormous historical importance in China, including its early relationship with Mao Zedong. Chongking and Chengdu together form a major central population center. In the South, Guangzhou (also known as Canton) and Hong Kong form a highly important economic center on the world’s stage. Also lying between Guangzhou and Hong Kong is the city of Macau.

For perspective, the straight line distance between Beijing and Hong Kong is 1,236 nautical miles, comparable to Los Angeles-Houston. But stepping backward with a broader look, if we compare China’s geography and population distribution to that of the US, consider a straight line drawn in the US from Chicago to New Orleans. Then compare that to a line drawn in China from Bautou in the North to Kunming in the South. The great majority of China’s population lies to the east of that Bautou-Kunming line. It is as though the entire population of the US were restricted to the Eastern portion, entirely East of a line from Chicago to New Orleans. Relocate all of the US cities of the Western side to the Eastern side of this line (cities such as Los Angeles, San Francisco, Seattle, Phoenix, and Denver) and then quadruple the population and have all of that in the Eastern side. In the three areas of concentration described above, the population density is between 520 people per square mile to more than 1,000 people per square mile. But that is covering the entirety of very large areas of the country, not just the major cities. (The population density of Metropolitan Los Angeles is 5,300 people per square mile.) China’s middle class is numerically larger than the middle class of the US (109 million compared to 92 million.) That said, as a percentage of the population, some 11% of all Chinese are considered to be middle class while 50% of the US population is middle class. At the same time, one out of six middle class people in the world live in China. Depending on what is used to “normalize” the economic statistics, China’s economy has already surpassed the economy of the US. and is now #1 in the world. For example, if we normalize GDP to that of the “Purchasing Power” of its citizenry, China beats the US by a wide margin. [1] China is developing its infrastructure at a staggering rate, far surpassing anything that the West has ever done or could conceivably do in the future. China is building is rail network such that in three years it will grow from 78,000 km today to more than 120,000 km in length. Sixty percent of that will be electrified. It is building airports at an astonishing rate, basically constructing entirely new large airports (capable of large airline operations) at a rate of eight airports every year. It will build some 800 new general aviation airports (hard-paved) between now and 2020. China is building a new airport in Beijing, named Daxing, to be the largest international airport in the world, having 7 runways and accommodating 100 million passengers per year. (In comparison, LAX with 4 runways accommodates 63 million per year.) By 2020, China’s airline industry will be the largest of all the nations in the world, pushing the airline industry of the US into second place, perhaps forever. More about that in Part Two. [1] What this means is that the cost of living in China is far less than that of the US. Money earned goes much further.  SkyWest Airlines has recently ordered 100 of the new Mitsubishi MRJ90 regional jets, adding 100 options for more. At the present time, these aircraft cannot be used for service with SkyWest’s Legacy airline affiliates (Delta Connection, American Eagle, and United Express.) Why? Does this foreshadow a major new shakeup of the regional airline industry? Japan’s Mitsubishi Aircraft Corporation (“MAC”) has been developing a new regional jet for the past fourteen years. This corporation is a partnership between the majority owner, Mitsubishi Heavy Industries and the minority owner, Toyota Motor Corporation. Following an earlier period of development, the MRJ concept was introduced in 2007. Since then, the MRJ has suffered significant setbacks, racking up nearly $1.28 Billion in development costs. To recoup this investment, Mitsubishi projects that it will have to sell as many as 400 MRJ aircraft. It is likely that China will present a strong marketing opportunity for sales of the Mitsubishi MRJ. According to an article published on August 27, 2018 by Aviation Week and Space Technology, MAC expects to sell 619 aircraft of the MRJ class to China in the next twenty years. The MRJ will be the first airliner designed and produced in Japan since the 1960’s, when it produced the YS-11, which was produced at a loss. Mitsubishi has developed two different models of the MRJ, the MRJ70, that has 69 to 80 seats, and the larger MRJ90, having 81 to 90 seats. There is no MRJ model under development that will be useful in the U.S. regional airlines 50-seat market. Both the MRJ70 and the MRJ90 are offered in three different versions: the Standard Model, the “ER” and the “LR” models. All but two of the six models run up against the “Scope Clause” that the U.S. Legacy carriers have with their pilot’s union. These Scope Clauses place a complete restriction on their Regional Airline Affiliates flying any aircraft with a maximum takeoff gross weight (“MTOGW”) of 86,000 pounds or higher. There have been conflicting reports about the MTOGW of the MRJ70, but according to the official Mitsubishi web site, the MRJ70 Standard comes in at 81,240 pounds and the MRJ70ER comes in at exactly 86,000 pounds. The MRJ70LR has a MTOGW of 89,000 pounds. All three of the MRJ90 models are well beyond 86,000 pounds MTOGW of the Scope Clauses. Orders for the MRJ70 model are few. In the U.S. market, Trans States has ordered 5, Sky West has ordered 7 and AeroLease has ordered 2. The MRJ90 is faring much better, with Trans States ordering 50 (with options for 50 more), Sky West ordered 100 (with 100 options) and AeroLease ordering 10 (with 10 options.) Even so, it will not be until mid-2020 that any of these aircraft will be delivered to the Regional Airlines. Mitsubishi makes some very aggressive claims in its MRJ sales literature. They say that the design is “optimized”, yielding the highest fuel efficiency, the lowest environmental impact, and the most passenger comfort among the 70 to 90 seat jets “ever to take flight.” Mitsubishi claims that the MRJ has the “lowest cost to operate of any aircraft in its class.” (This includes fuel burn and maintenance cost.) Among other claims, Mitsubishi states that its “advanced aerodynamics” produces a low-drag fuselage and tail cone, a streamlined nose, and an optimized winglet. The MRJ has a full fly-by-wire flight control system, which is arguably the most advanced in this regional jet class. Importantly, the MRJ uses the newly developed Pratt & Whitney Geared Turbofan engine, the MRJ70 using the PW1215G model and the MRJ90 using the PW1217G model. Mitsubishi claims a 20% lower fuel burn than comparable engines in this thrust class (15,600 to 17,600 pounds thrust.) One of the negative aspects of the MRJ70 and the MRJ90 is its limited range. The MRJ70 Standard has a range of only 1,020 nautical miles. The MRJ70ER has a range of 1,670 nautical miles and the MRJ70LR has a range of 2,020 nautical miles. The three versions of the MRJ90 have ranges of 1,150, 1,550, and 2,040 nautical miles respectively. In comparison, the Airbus A220-100 has a range of 3,100 nautical miles with a passenger capacity of 108 to 133 passengers. The Embraer E2 models have range capability starting at 2,150 nautical miles and going up to 2,450 nautical miles. So, even the “long range” versions of the MRJ do not meet the range of the most limited Embraer E2 models. However, considering that the target market for the MRJ is the regional airline market, and given that this market generally is a short-to-medium stage length market, the range limitation may not be as damaging as it seems. Today, the U.S. regional airlines operate jet aircraft that are the products of Canadair/Bombardier (now owned by Airbus) and Embraer (soon to have 80% Boeing ownership.) No Japanese designed and manufactured airliner has been operated in the U.S. since around 1982, when Mid-Pacific Airlines operated the YS-11 in Hawaiian service. (American Eagle also operated the YS-11.) Mitsubishi has commercial agreements with Boeing wherein MAC’s majority owner manufactures fuselage panels for the B777 and wingboxes for the B787, among other issues involving support. Now that Boeing will be supporting Embraer’s RJ products, how will that apparent conflict with the MRJ work itself out? Will Japan penetrate the U.S. aircraft market as it has in the automobile market? Given Toyota’s involvement with Mitsubishi and the MRJ, and given the top-of-the-line marketing claims of MRJ, can this happen? Will Mitsubishi move to produce a replacement for the ERJ145?  |

Categories |

RSS Feed

RSS Feed

Live Chat Support

×

Connecting

You:

::content::

::agent_name::

::content::

::content::

::content::